.svg?format=webp)

.jpg%3Fformat%3Dwebp&w=3840&q=75)

.jpg%3Fformat%3Dwebp&w=3840&q=75)

Top VHIS winner¹

vPrime Medical Plan

Full cover² for a series of hospitalisation and surgical expenses, up to HK$16.5 million per policy year and also be used for tax deductions

I am applying for

Gender

Each Insured Person can only be covered under one NobleCare Premier Medical Plan, Glory GlobalCare Medical Plan, vPrime Medical Plan, vPrime Signature Medical Plan, vTheOne Medical Plan, TheOne Medical Solution or TheOne Medical Solution Rider.

Choose a plan

Have a promo code?

Each Insured Person can only be covered under one NobleCare Premier Medical Plan, Glory GlobalCare Medical Plan, vPrime Medical Plan, vPrime Signature Medical Plan, vTheOne Medical Plan, TheOne Medical Solution or TheOne Medical Solution Rider.

All premiums are calculated on standard rates and this quote is for reference only. The premium levy, which we’re obliged to collect for the Insurance Authority, is payable in addition to the actual premium to be paid.

Before proceeding, please confirm you understand this product’s features and that it fits your need(s) and affordability.

If your application is approved on or after 2 February 2026, your policy will be issued at a new premium (please refer to Company website for the new premium available on or after 2 February 2026). An updated modal premium for first Policy Year will be shown in policy schedule after policy issuance.

Why do you need VHIS?

vPrime Medical Plan (“vPrime”)3 provides full cover2 for a series of hospitalisation and surgical expenses up to HK$16.5 million per Policy Year and without Lifetime Benefit Limit for your future protection. vPrime3 is a “5-star”4 VHIS, not only alleviating your medical burden, but also allowing tax deductions5!

"5-Star"4 Medical Insurance Plan, providing comprehensive coverage for you and your family's medical needs, received various awards and accolades, including:

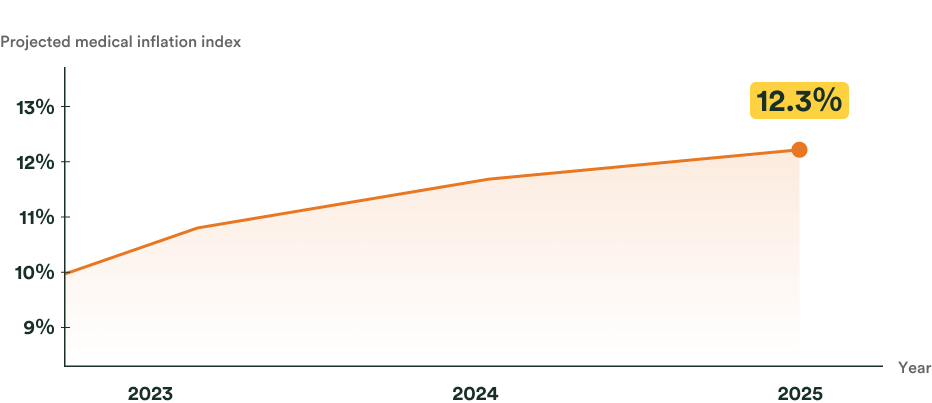

Is consulting a doctor getting more expensive? vPrime can help you!

Projected Medical Inflation Index in the Asia-Pacific Region7

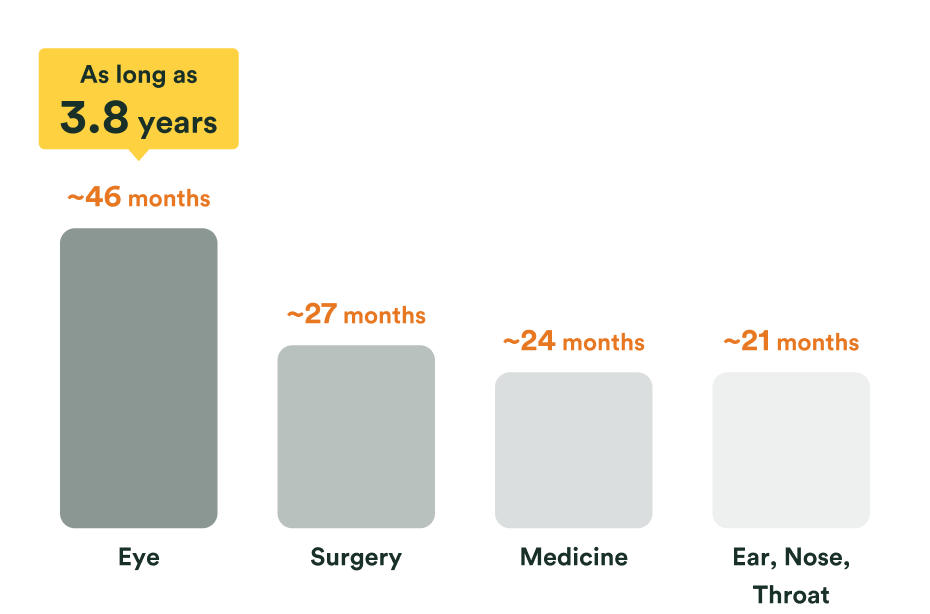

Long waiting times at public hospitals? vPrime can help you!

Waiting Time for New Case Booking for Specialist Out-patient Services in Hong Kong public hospitals8

Although public hospital fees in Hong Kong are relatively affordable, the waiting time for new case booking for specialist out-patient service can be as long as 3.8 years, which may lead to missing the best opportunity for treatment!

Real life story

In her 30s, was suddenly diagnosed with late-stage nasopharyngeal cancer and chose proton therapy and chemotherapy. After a year of treatment, she successfully recovered!

vPrime3 provides full cover2

PREMIER THE ONEcierge24,25 provides you with one-stop support

vPrime3 provides full cover2

Using medicines to destroy cancer cells.

Proton therapy is a type of radiation treatment that significantly reduces radiation exposure to surrounding healthy tissues and organs compared to traditional methods. This approach minimizes damage to nearby tissues, lowers the risk of common complications and side effects, and helps preserve quality of life.

vPrime3 provides full cover2 for Proton Therapy

PREMIER THE ONEcierge24,25 provides you with one-stop support

(852)8120 9066

vPrime3 provides full cover2

Others

FWD Care recovery plan 24,25

How does vPrime help you save on taxes?

"Voluntary Health Insurance Tax Deduction" refers to the qualifying VHIS premiums that can be claimed as deductible expenses in your tax return. These amounts are subtracted from your taxable income, helping to reduce your tax burden indirectly5.

vPrime is designed in accordance with the VHIS framework recognised by the Health Bureau and is a qualifying VHIS plan. Its premiums are therefore eligible for tax deduction 5. The actual tax savings will depend on your marginal tax rate and the actual premium amount.

How is the VHIS tax-deductible amount calculated?

The formula for calculating the VHIS tax-deductible amount is: Tax-deductible premium (capped at HK$8,000) × your marginal tax rate = actual tax savings.

For example, if your VHIS tax-deductible premium is HK$8,000 and your marginal tax rate is 17%, the tax saved would be: HK$8,000 × 17% = HK$1,360.

What is the maximum VHIS tax-deductible amount?

The maximum VHIS tax-deductible amount is HK$8,000 per eligible insured person per year. However, this does not mean your tax bill will be reduced directly by HK$8,000. The actual VHIS tax-deductible amount will depend on your progressive tax band (ranging from 2% to 17%).

How is VHIS tax deduction calculated for family members?

If you take out a qualifying VHIS policy for yourself and your specified relatives, each insured person can enjoy a maximum VHIS tax-deductible premium of HK$8,000 per year, with no limit on the number of insured persons.

Specified relatives generally include:

- Your spouse

- Your children

- Your parents, grandparents or maternal grandparents aged 55 or above (including your spouse's parents and grandparents)

For example, if you enrol yourself and three additional family members in vPrime, and your personal tax rate is 17%, you may claim VHIS tax‑deductible premium of up to HK$32,000 per year. Your potential tax savings could be: HK$32,000 × 17% = HK$5,440.

What’s special about vPrime?

Full cover for a series of hospitalisation and surgical expenses, up to HK$16.5 million per Policy Year and without Lifetime Benefit Limit

With the rapid advancement in medical technology, the biggest fear is not being ill, but being unable to afford the treatment cost!

approx. HK$270K9

Out-of-pocket medication cost in the public hospital

approx. HK$1.29M9

Overall treatment cost in the private sector

vPrime3 provides up to HK$16.5 million per Policy Year for eligible medical expenses and cash benefits, and without Lifetime Benefit Limit!

Utilise 6 deductible options to make premiums more affordable

| Deductible options10 | Monthly premium at 1st year* (based on ANB31) |

|---|---|

| HK$0 | HK$991 |

| HK$16,000 | HK$326 |

| HK$25,000 | HK$280 |

| HK$50,000 | HK$213 |

| HK$100,000 | HK$167 |

| HK$250,000 | HK$135 |

Deductible to be waived for designated crises

Relieving the financial burden of treatment, allowing you to focus more on healing and recovery.

(Age next birthday: 37)

has applied for vPrime3 – Deductible HK$250,000

Policy effective date – 1 September 2024

| Treatment expenses for breast cancer |

HK$ 180,000 12 |

|---|---|

| minus Deductible10 |

If unfortunately diagnosed with a designated illness13, the deductible10will be waived under First-dollar coverage – Deductible waived for designated crises10,13,14.

|

| Total payout amount | HK$180,000 |

Innovative cash benefits in the VHIS market provides additional financial support

In specified circumstances, additional cash benefits will be provided.

| Deductible options10 | HK$0 | HK$16,000 | HK$25,000 |

|---|---|---|---|

| Cash benefits | Cash benefits amount | ||

| (1) Day case procedures15 | (i) Designated Day Case Procedure(s) performed at a Designated Healthcare Services Provider6 or in mainland China:

HK$3,600 per procedure [doubled up] [Market-first in the VHIS+]

(ii) For any Day Case Procedure(s) other than designated Day Case Procedure(s) performed Payable once per day for a maximum of 1 Day Case Procedure in accordance with benefit item (i) or (ii) as specified above | ||

| (2) Reimbursement paid by other insurance companies16 | HK$1,000 per day of Confinement Max. 60 days per Policy Year | ||

| (3) Admission to standard ward room in HK private hospital17 | HK$1,700 per day of Confinement Max. 30 days per Policy Year | ||

| [Market-first in the VHIS+] (4) Major and complex surgeries18 | HK$6,000 per major surgery HK$12,000 per complex surgery (Max. 1 major or complex surgery per day) | ||

| [Market-first in the VHIS+] (5) Confined in Intensive Care Unit in HK19 | HK$12,000 per Confinement | ||

| Deductible options10 | HK$50,000 | HK$100,000 | HK$250,000 |

|---|---|---|---|

| Cash benefits | Cash benefits amount | ||

| (1) Day case procedures15 | (i) Designated Day Case Procedure(s) performed at a Designated Healthcare Services Provider6 or in mainland China:

HK$3,600 per procedure [doubled up] [Market-first in the VHIS+]

(ii) For any Day Case Procedure(s) other than designated Day Case Procedure(s) performed Payable once per day for a maximum of 1 Day Case Procedure in accordance with benefit item (i) or (ii) as specified above | (i) Designated Day Case Procedure(s) performed at a Designated Healthcare Services Provider6 or in mainland China:

HK$1,800 per procedure [doubled up][Market-first in the VHIS+]

(ii) For any Day Case Procedure(s) other than designated Day Case Procedure(s) performed at a Designated Healthcare Services Provider or in mainland China; or any Day Case Procedure(s) performed at a non-Designated Healthcare Services Provider outside mainland China: Payable once per day for a maximum of 1 Day Case Procedure in accordance with benefit item (i) or (ii) as specified above | |

| (2) Reimbursement paid by other insurance companies16 | HK$1,000 per day of Confinement Max. 60 days per Policy Year | HK$500 per day of Confinement Max. 60 days per Policy Year | |

| (3) Admission to standard ward room in HK private hospital17 | HK$1,700 per day of Confinement Max. 30 days per Policy Year | HK$900 per day of Confinement

Max. 30 days per Policy Year | |

| [Market-first in the VHIS+] (4) Major and complex surgeries18 | HK$1,200 per major surgery HK$2,500 per complex surgery (Max. 1 major or complex surgery per day) | ||

| [Market-first in the VHIS+] (5) Confined in Intensive Care Unit in HK19 | HK$2,500 per Confinement | ||

Up to 30% no claims premium discount

Maintain good health to enjoy higher discounts and be rewarded for a healthy lifestyle.

| No claims period immediately prior to the Policy’s Renewal20 | No claims premium discount (Applicable to Renewal20 premium) |

|---|---|

| 2/3/4 consecutive Policy Years | 15% |

| 5 consecutive Policy Years and thereafter | 20% |

| Number of eligible policies21 | Extra no claims premium discount22 under your eligible policies21 |

|---|---|

| 2 or 3 | 2.5% |

| 4 | 5% |

| 5 or above | 10% |

| FWD vPrime3 | Company A VHIS | Company P VHIS | |

|---|---|---|---|

| Self Application | 20% | 15% | 15% |

| Application for self and family | 30% |

Other product highlights

The protection you need to safeguard your health

Covering unknown Pre-existing Conditions at the time of application, including Congenital Condition(s)

FWD Care Prestige health assistance services24,25 for the support you need

Enhanced benefits to support you on your road to health again

Extra support for stroke rehabilitation

A trusted plan with VHIS features

vPrime3 is certified by the Government and Policy Holders are eligible for tax deduction5

Guaranteed Renewable20 up to Age 100 of the Insured Person

During and after pregnancy, taking care of the health of both mothers and babies

Pregnancy complications benefit

Free coverage for newborns

Child development benefit

Worry about failure to get reimbursed by an insurance, and cannot claim the full cost of hospitalisation or treatment expenses31? Do not want to worry about the claim process?

Cashless Facility Service for hospitalisation and day case procedures

Cashless Facility Service24,30 = Receiving treatment without having to make a payment from the start to completion31

Hospital network covering Pan-Asia regions for Cashless Facility Service for hospitalisation:

All HK private

hospitals (13 in total)32,33

All 3A hospitals

Apart from hospitalisation, you can also enjoy Cashless Facility Service for day case procedures:

General Information

Standalone Plan

Age 0 (from 15 days) – 80 (attained age)

Guaranteed yearly renewable20 to age 100 (attained age)

- Based on Insured Person’s attained age at issue

- Renewal20 premiums are non-guaranteed and will be determined annually and according to the Insured Person’s attained age at the time of renewal20

To Age 100 (attained age)

This platform offers Monthly and Annual premium payment mode

Policy holder can contact FWD Customer Service to amend premium payment mode after policy is effective

HKD

| Deductible10 options | certification numbers |

|---|---|

| HKD0 | F00045-01-000-05 |

| HKD16,000 | F00045-02-000-05 |

| HKD25,000 | F00045-03-000-05 |

| HKD50,000 | F00045-04-000-05 |

| HKD100,000 | F00045-05-000-03 |

| HKD250,000 | F00045-06-000-03 |

vPrime Medical Plan is underwritten by FWD Life Insurance Company (Bermuda) Limited (incorporated in Bermuda with limited liability) ("FWD Life/ FWD/We"). This eCommerce Platform is operated by FWD Financial Limited ("FWD Financial"). FWD Financial is an appointed and licensed insurance agency of FWD Life.

The product information in this website is for reference only and does not contain the full terms and conditions, key product risks and full list of exclusions of the policy. For the details of benefits and key product risks, please refer to the product brochure; and for exact terms and conditions and the full list of exclusions, please refer to the policy provisions of vPrime.

This product is available for online or offline application.

Applicable for online application:

• I (and the Insured person if applicable) am a permanent HKID card holder with a Hong Kong residential address.

• Currently in Hong Kong at the time of making this application.

• I will not or have no intention to live or work outside Hong Kong or home country over 183 days in the coming 12 months.

• I am not a holder of the People’s Republic of China Resident Identity Card.

Note: Online applicants will be requested to visit FWD Insurance Solutions Centres under the following circumstances: 1) Collection of policy documents upon issuance of policy; 2) Cancellation of policy during the cooling-off period; 3) Change of beneficiary; or 4) Full surrender. Under specific circumstances, we may request online applicants to visit FWD Insurance Solutions Centres for identity verification.

Unable to complete the online application or not exactly what you need?

If you require broader coverage, a higher insured amount, or have other inquiries, please contact us.

Frequently Asked Questions About VHIS

What is VHIS?

The Voluntary Health Insurance Scheme (VHIS) is a policy initiative introduced by the Health Bureau. VHIS products are individual indemnity hospital insurance products complied with the minimum requirements set out by the Health Bureau. It aims to enhance the protection level of individual indemnity hospital insurance products, provide the public with an additional choice of using private healthcare services through individual indemnity hospital insurance, and relieve the pressure on the public healthcare system in the long run. VHIS also allows you to enjoy tax deduction5.

Why do I need VHIS?

Facing sudden illnesses, taking out medical insurances earlier can provide you with protection, allowing you to easily handle hospitalisation and surgical expenses. One of the benefits of choosing VHIS is that it can cover unknown pre-existing conditions at the time of application (subject to relevant waiting periods) and guarantee renewal up to the age of 100 (attained age). Additionally, the plan must comply with the government's standard terms and conditions, minimum coverage, and benefit limits, allowing you to enjoy higher protection and transparency.

What is the difference between a medical insurance plan in general and VHIS?

The terms of medical insurance plans in general vary by insurance companies, while VHIS is certified by the government and must be complied with several standard product requirements to enhance consumer protection. Besides, VHIS is eligible for tax deduction5.